Digital lending in India is undergoing a transformative phase in 2024, driven by the government’s digitization initiatives and the emergence of innovative FinTech companies. The sector is expected to exceed $720 billion by 2030, with a significant contribution from products like Buy Now Pay Later (BNPL), Invoice-based lending, and P2P lending. A key factor in this growth is the increasing financial and digital literacy, especially in rural areas, where access to organized credit was previously limited. The widespread adoption of smartphones and high-speed internet has made digital lending products accessible to over half of India’s population.

The integration of Aadhaar and eKYC has simplified consumer access to digital lending, benefiting even the MSME sector, which forms a substantial part of India’s GDP. The India Stack, a comprehensive digital public infrastructure, has been pivotal in reducing banking costs and enhancing access to financial services, thereby transforming India’s cash-based economy. This has allowed digital lenders to significantly reduce user verification costs and offer real-time mobile payments.

FinTechs are leading the way in leveraging alternative data for credit assessments, enhancing operational efficiencies, and addressing credit gaps with inclusive product offerings. The collaboration between banks, NBFCs, and FinTech startups is fostering innovation and efficiency in the digital lending space. As we move into 2024, this synergy is expected to deepen, driving further innovation and meeting the diverse credit needs of Indian households and businesses.

In this evolving landscape, earned wage access (EWA) plays a crucial role. EWA services, like those offered by KarmaLife, provide immediate access to earned but unpaid wages, empowering workers to manage financial emergencies and reduce reliance on high-cost credit options. This model is particularly relevant in India, where a significant portion of the workforce is engaged in gig and blue-collar jobs. EWA is not just a lending product but a financial wellness tool, promoting responsible borrowing and financial stability among workers. As digital lending grows, EWA is poised to become an integral part of India’s financial inclusion story, offering a unique blend of accessibility, convenience, and empowerment to the workforce.

KarmaLife’s EWA solutions are tailored to meet the specific needs of India’s blue-collar gig workers, a demographic that has traditionally been underserved by conventional financial institutions. By providing access to wages as they are earned, KarmaLife addresses a critical gap in the financial ecosystem, offering a lifeline to those who may otherwise resort to unorganized or high-interest credit sources in times of need. This approach not only alleviates immediate financial stress but also fosters a culture of financial responsibility and planning.

Moreover, KarmaLife’s innovative use of technology aligns perfectly with the digital transformation in India’s financial sector. By leveraging artificial intelligence, strong data crunching models and digital platforms, KarmaLife makes EWA services easily accessible, even in remote areas. This accessibility is crucial in a country where smartphone penetration is rapidly increasing, bringing more users into the digital fold.

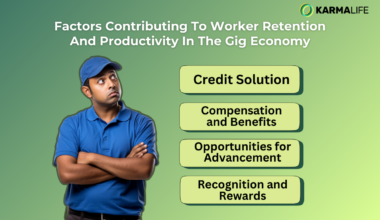

In addition to providing financial relief, KarmaLife’s services also contribute to a broader economic impact. By empowering workers with immediate access to their earnings, there is a potential increase in consumer spending, which can stimulate local economies. Furthermore, the sense of financial security and independence that EWA provides can lead to improved worker satisfaction and productivity, benefiting employers and the economy at large.

As we look towards 2024 and beyond, the role of companies like KarmaLife in India’s digital lending space becomes increasingly significant. By bridging the gap between traditional banking services and the needs of the modern workforce, KarmaLife is not just a participant in the digital lending revolution; it is a catalyst for a more inclusive and equitable financial future in India.